When it comes to obtaining returns, being in the right place at the right time is as important as having the required skills: chance and capability.

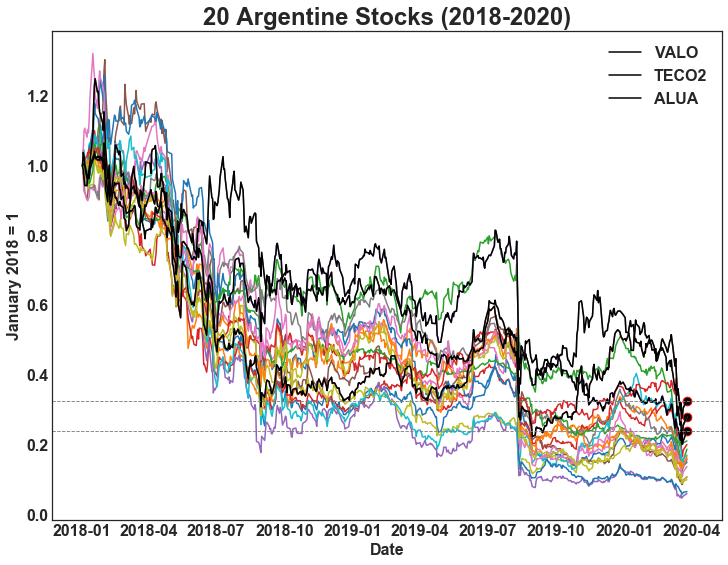

Let’s imagine a well-prepared investor who is able to choose the three Argentine stocks that will perform best in the future. These stocks are Grupo Financiero Valores, Aluar and Transportadora de Gas del Sur. The problem is that the investor is in January 2018, during the prelude to Argentina’s worst crisis since 2001.

The result of investing in these three stocks is a loss of 71.8% throughout two and a half years, which is enough to dampen any investor’s spirits.

Likewise, a not-so-proficient investor who lags behind the MERVAL Index on a 5% yearly basis, but who begins to invest in June 2002, will get disproportionately high results in the following five years.

Stocks move following herd behavior. It is useful to study them in detail so as to avoid falling behind the market and even to exceed its performance. However, the results are largely explained by the overall market trend, not by the selected stocks.

This maxim applies especially for Argentina due to the concentration of the listed companies in the energy and financial sectors, which reduces the possibilities of diversification.

In finance, this idea is summarized by “don’t pray for alpha, pray for beta”, which means “don’t pray for beating the market, pray that the market won’t stop climbing”.

Probabilities and the Kelly criterion

History does not transpire homogeneously, it is plagued with fortuitous circumstances that change the course of events. The scientist John Kelly became known in 1956 for creating a formula to establish the optimal bet amount in games with positive expected outcome. Once the validity of his formula was mathematically proven it became widely used in the financial markets.

Imagine a game where you flip a coin. Heads: you double the bet; Tails: you lose half of it. You can flip the coin as many times as you want.

Betting all the capital on each coin toss could lead to an impossible-to-overcome situation after a losing streak. Conversely, a small bet means losing potential profit in a game that clearly has a positive expected value, since you either double the investment or you lose just half of it. Somewhere in the middle is the optimal amount to bet.

According to Kelly’s formula, in this scenario we should bet 50% of our capital on each flip. This way you maximize the expected profit after an adequate amount of coin tosses – remember this has mathematical proof.

Kelly = (probability of winning/potential loss) – (probability of losing/potential profit)

Argentina’s Merval Index can be considered today as one of these flipping coins. It’s impossible to know what will happen to the economy and the stock market, since even the best future scenario analysis are vulnerable to any sudden government regulation that changes the game rules, or simply to a casual or unexpected event that shapes its destiny.

According to the bullish and bearish cycles, we can infer that if the MERVAL Index returns to its long-term average, you can earn a 126% return. On the other hand, if the market keeps falling and goes beyond the low of March, we might have to close the position at a stop loss of ‑50%.

Supposing the probabilities of both scenarios are 50%, Kelly suggests we should invest 60% of the bankroll.

If we stress-test this, we could consider only a 40% probability of a positive outcome and 60% odds of a negative outcome. The expected value is still positive since (40% * 126%) – (60% * 50%) = 20%. However, in this scenario Kelly’s criterion reduces the optimal bet size to 32% of the bankroll, almost half than before.

That being said, most investors will not tolerate the volatility and the drops that come when investing 32% of the capital on argentine stocks, which is why referring to ‘a half’ or ‘a quarter of’ a Kelly is a common practice in the market. This also has to do with the fact that positively correlated assets also reduce the optimal kelly.

Summing up

If we find current MERVAL values enticing enough to try our luck, and we use the Kelly criterion to establish how much to invest, we should buy Argentine stocks for 32% of the capital we have set aside for risky bets. We could also take a fraction of that amount to reduce the volatility and potential losses of the portfolio.

If we live long enough to see the MERVAL climb and fall in several additional cycles, then this will be the proportion that should produce the best outcome.

What stocks should we invest in?

Art merchants developed a technique that made them filthy rich without the need to know beforehand what paintings represented a sound investment. This paper by Horizon Research Group discusses in detail how a number of marchands d’art of the 19th and 20th centuries ended up owning massive collections of masterworks by Picasso, Matisse, Klee and others worth hundreds of millions of dollars.

Basically, they bought as many paintings as they could, even works that had not yet been painted and which they had no idea what they would look like. They had understood that the value of art is subjective and that there is no way to know what trends will set the price after 25 or 50 years.

Unlike the cycles that the financial markets undergo, when the value of a painting starts increasing, it generally sets a trend that will persist in time.

The mathematics for this case are simple. Let’s imagine a static, non-rebalancing portfolio made up of three paintings. Let r be the annual return of each painting and n the number of years. The value of the collection will be defined as:

Collection value = Painting A * (1 + r)ⁿ + Painting B * (1 + r)ⁿ + Painting C * (1 + r)ⁿ

Following this logic, it is not important whether a part of the investment loses half of its value. Since there is no rebalancing, the best investment will boost its participation and the profit of the collection will slowly converge to the performance of the best painting. Merchants had discovered a precursor to the idea of index investing.

Something similar —though not identical— occurs in financial markets. According to a report published by JP Morgan, the Russell 3000 index multiplied its value by 49 between 1980 and 2014. However, 40% of the companies suffered losses greater than ‑70% and could never recover.

In addition, 64% of the stocks underperformed the index and only 7% had an outstanding performance that explained most of this index’s climb.

The probability of ending up owning that 7% is low. On the contrary, think about the 64% of underperformers.

As for the MERVAL Index, I believe we all agree on the future being somewhat bleak for power companies whose income depends on regulated tariffs, and that maybe banks and import-substitution industries will outperform. This vision is based on solid ground but, once again, the winds of fate might veer us off course.

The moral of the story is that proper diversification across sectors and companies increases the probabilities of ending up owning the (today unknown) future outperformers that will save the overall portfolio performance. All is left to do is to wait for the future to tell us whether we are in the right place at the right time.

Thanks for reading!

2 respuestas

Muy buen análisis, Camilo. Te escuché en el podcast con Fede Tessore y me decidí a seguir tus análisis a partir de ahora. Tenés un seguidor más!!!

Gracias Cristian!